Financial Services Innovation Coalition: Expanded Debt Relief Access Is An Important Solution to America’s Affordability Crisis

As the United States celebrates 250 years of independence, most Americans do not believe their own financial freedom is still possible. In fact, there is no longer a consensus that hard work and initiative are all it takes to get ahead. According to an Associated Press poll, only one-third of Americans feel the American Dream holds true today.

A new Financial Services Innovation Coalition (FSIC) report offers insight into why so many Americans feel it is impossible to get ahead: debt is no longer a temporary mechanism prudently used to buy a home or finance an education. Rather, it is the only way many Americans can afford everyday life.

In an economy where debt is a means of financial survival — and where financial stress is taking a toll on mental health— consumers need access to options, including debt relief, which provides important consumer protections and a regulated alternative to bankruptcy.

How Debt Became a Means of Survival

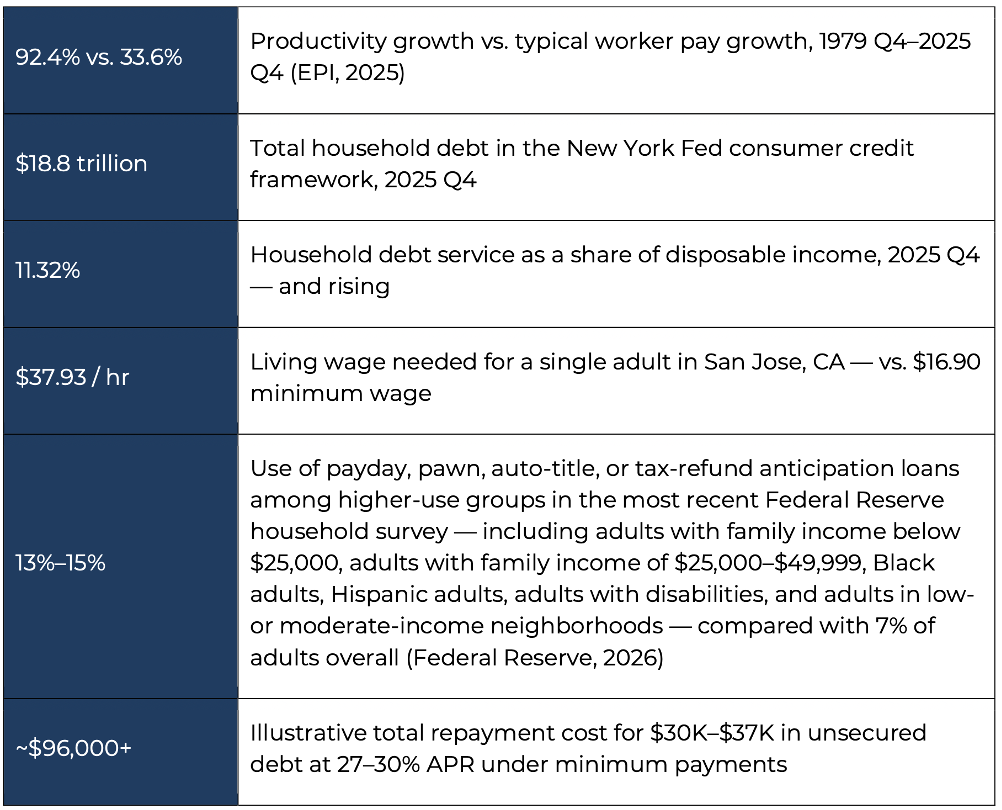

In the United States today, a person can do everything right and still fall behind financially. Since 1979, worker productivity has grown 92.4 percent while typical worker pay has risen only 33.6 percent.

“The result is a widening, structural gap between what households earn and what they must spend to remain financially stable,” the report says. This gap means Americans are using debt to bridge rent burdens, pay for healthcare, replace volatile income, buy food, and even finance transportation to work.

FSIC illustrates how quickly this debt can become all-consuming. As shown in the graphic below, a household carrying $30,000–$37,000 in unsecured debt at a 27-30 percent interest rate making near-minimum payments will pay more than $96,000 total — more than three times the original balance — and remain in debt for roughly three decades.

The burden may be about to get worse, too. FSIC warns new technologies like artificial intelligence may “amplify financial instability,” accelerating debt dependence. How can policymakers help Americans climb out of this spiral? FSIC offers some ideas, including expanding access to debt relief.

Why Is Access to Debt Relief So Important?

The FSIC report concludes that debt relief serves as an important segment of financially distressed consumers who may not be well served by other available options.

According to FSIC, a household carrying a $6,000 credit card balance at a 30 percent annual percentage rate making near-minimum payments can remain indebted for well over a decade. Under this scenario, total interest payments would rival or exceed the original principal.

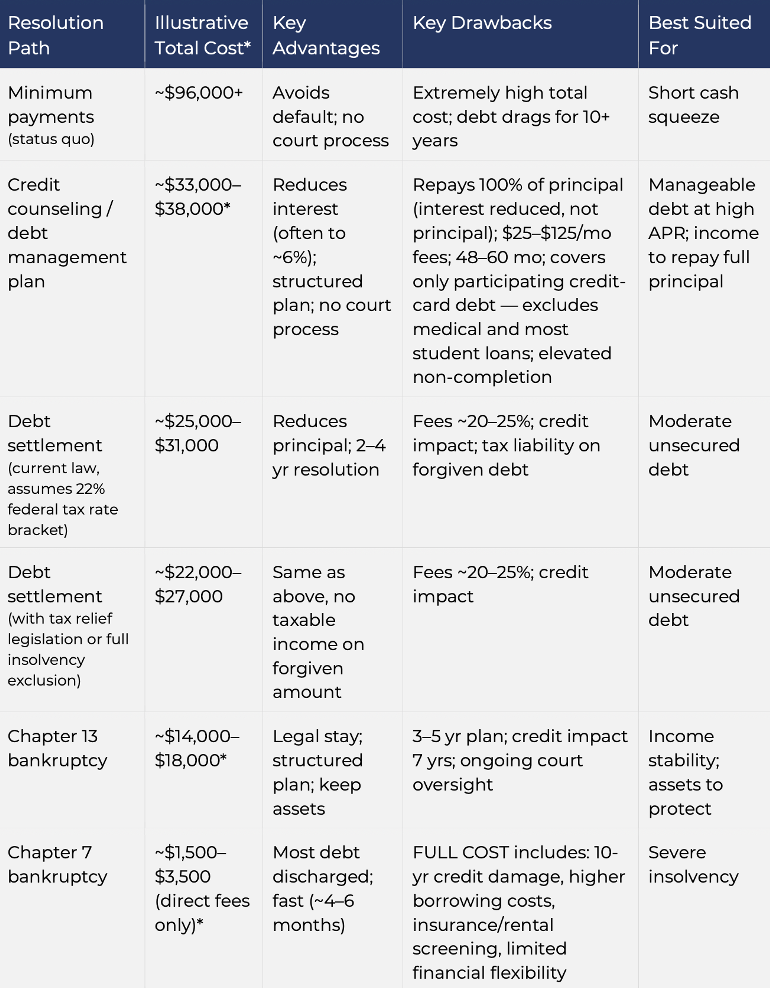

Unfortunately, “when unsecured debts become unmanageable, households generally face a limited set of resolution paths,” FSIC explains. Bankruptcy is one option, but it can come with major drawbacks. Credit counseling is another, but, as the graphic below demonstrates, it is a more expensive option for consumers than debt relief because it does not reduce the amount of principal owed and typically comes with up-front or monthly fees, despite its non-profit status.

Debt relief is a proven, federally regulated process that allows consumers facing financial hardship to resolve unsecured debts, such as credit cards, personal loans, or medical bills, for less than what they owe. ACDR accreditation ensures that companies that provide debt relief services go above and beyond already robust state and federal protections, giving consumers added confidence that they are in control and on the right path to regaining their financial freedom.

To illustrate how debt relief helps consumers, FSIC offers a family with $18,000 in credit card debt, limited savings, and a stable (though modest) income. By leveraging debt relief, this family can eliminate its debt in two to four years and for about 32 percent ($5,760) less than they owe. With credit counseling, that family may be able to reduce interest rates or negotiate the repayment timeline but would be unable to reduce the principal balance.

Over the past several years, family budgets have been squeezed by high prices for essentials and crushing interest rates. While debt relief is not a substitute for responsible lending and financial planning, it provides consumers an important pathway to restoring financial stability.